Annexes

Annex 1: Categories of Existing Platform Arrangements

Development partner coordination platforms serve as mechanisms to help governments develop comprehensive public investment projects/programs, prioritize them and match development partners to needs based on their comparative advantages. Successful coordination platforms are usually characterized by strong government ownership, transparency and consultation with participants in the platform. (See Box 1 on the Rwandan example.)

Box 1: Rwanda - Development Partner Coordination

The Government of Rwanda has developed a successful development partner coordination mechanism that has several features of the proposed country platforms. The Government’s long-term development goal is to transform Rwanda into a middle-income country, through a series of five-year development strategies. It has a strong emphasis on sustainability and inclusivity. Development partner support is achieved through a coordinating mechanism that embodies several principles of good governance – strong country ownership with coordination by the Minister of Finance; the alignment of partners around a coherent development strategy; mutual accountability of Government agencies and the development partners; transparency; and a system within Government (including local government) of managing for development results. This coordination mechanism also facilitates an agreed division of labor among the development partners, to reduce transaction costs and ensure engagement in line with comparative advantage. It has resulted in greater focus by each development partner and continuity in their programs, and scale efficiencies. To date, it involves largely official development partners and NGOs but the Government is now focusing on incorporating DFIs and the private sector. Doing so will broaden its reach. Convergence among all the development partners around core standards would also enhance development impact and sustainability.

Reconstruction platforms tend to be formed to address specific post-conflict or fragility needs. Two recent examples are: Ukraine reconstruction activity, in the immediate aftermath of the conflict, which was led by the EBRD and the EU with the involvement of the EIB and the IBRD/IFC as well as bilaterals and philanthropies; and the Jordan Response Plan for the Syrian crisis which brings together the main MDBs, bilaterals, UN agencies and NGOs.

Single sector platforms have been successful in bringing together projects for private sector financing alongside official financing. The Colombia 4G program and the associated DFI Financiera de Desarrollo Nacional (FDN) is a successful example, involving an investment program to create a nationwide toll road network through up to 40 different public private partnerships (PPPs) with mostly greenfield infrastructure projects. Indonesia’s national slum upgrading program is also instructive (see Box 2). The Brazilian Private Sector Participation Facility, a joint effort of IDB, IFC and BNDES, is another platform designed to enhance private sector participation in infrastructure by helping to structure projects from technical and economic feasibility studies to financial closing. A program/platform for ports in Ukraine was just started by the EBRD and the IFC.

Box 2: Indonesia - National Slums Upgrading Program (NSUP)

The Government of Indonesia has taken a ‘platform approach’ to the financing of some of its major development programs. This has enabled the Government of Indonesia to bring together financing consortiums of MDBs as well as the government’s own program budgets. An example of this approach is the “National Slums Upgrading Program (NSUP),” which is a nation-wide program to improve urban infrastructure and services for 29 million Indonesian slum residents living in 239 cities throughout the country. The NSUP included financing from four MDBs (IBRD, IsDB, AIIB and ADB) and from community and government sources. The World Bank took the lead role in preparing the project and coordinating the financing. Project implementation is being overseen by a common project management unit and the project is applying the same policies and safeguards to all investments financed under the project, regardless of the source. This is an example of how a platform approach can be country-driven, attract financing at scale, build government capacity, use a set of common standards and bring together all tiers of government. Early evidence also indicates that it has improved the quality of government expenditures in a critical area for sustainable and inclusive growth. While this approach exclusively involved the Government and the MDBs, it does illustrate some clear advantages of taking a platform approach to development financing.

Source: World Bank staff and EPG secretariat

Global/regional infrastructure platforms are relatively new initiatives and have embodied aspects of the platform approach for infrastructure finance globally.

-

The Global Infrastructure Facility (GIF) is a partnership among governments, MDBs, private sector investors, and financiers to support governments in bringing well-prepared and structured projects to the market. It offers four services: infrastructure project prioritization, project preparation support, preparation of transaction documentation, and support through the process of financial closure.

-

The AfDB is developing the Africa Investment Forum (AIF) – a multi-stakeholder, multidisciplinary regional platform. The AIF is designed to screen and enhance projects, attract co-investors, reduce intermediation costs, improve the quality of project information and documentation, and increase active and productive engagements between African governments and the private sector. The objective is to offer access to bankable, de-risked projects within an enabling environment.

-

The Western Balkans Investment Framework (WBIF) is a multi-stakeholder, governmentled coordination platform – including beneficiary governments, IFIs, 20 bilateral donors and the European Union (EU) – which supports the socio-economic development of the Western Balkans region.

Annex 2: Building a Large and Diversified Asset Class of Developing Country Infrastructure

There is large scope and a real need to mainstream infrastructure financing/investments into a recognized asset class to catalyze the participation of institutional investors. This can be achieved by developing simple, standardized instruments that allow investors to invest on a portfolio rather than an individual loan/entity basis. Thus far there have been promising but piecemeal efforts to structure investible products for private investment that lack the necessary scale. There are major possibilities for strong multipliers.

To achieve the scale of an asset class and meet vast development needs, risk exposures have to be standardized and pooled from across the MDB system, into securitization or fund structures that enable easier investor access. Non-sovereign loans, infrastructure-related and others, would be a good group of assets with which to start. In the MDB system alone there are US$200-300 billion of such loans, which offers a critical mass for institutional investors. Including an aggregation of commercial bank loans would lead to much larger asset class (see two paragraphs down).

Individual MDB loans and portfolios of loans can potentially be transferred via a clean sale to private investors, in other words a complete transfer of the loan exposure to the private investor. MDBs are best placed to manage country and construction risk during the early phase of an infrastructure project, and hence should “hold” the loan during this phase. This early phase also coincides with the period when the MDBs add the most value. Upon completion of construction, the risk of the investment is reduced substantially and can be sold with the MDB retaining no interest in the investment. Should private investors demand slightly higher returns than what the MDBs price into the loan, a step-up pricing feature can be considered, such that loans have lower pricing during the construction phase but which are subsequently raised at project completion to commercial rates.

Beyond the loans originated by MDBs and bilateral agencies, the pool can be expanded to include commercial banks’ infrastructure loans or debt issued by commercial banks. This frees up balance sheet space or provides funding for commercial banks to extend new infrastructure loans. The growth of green bonds and green bond funds is another opportunity for MDBs and commercial banks to originate infrastructure loans that responds to the needs of institutional investors.

- An example is the IFC-Amundi Green Cornerstone Bond Fund, a US$2 billion initiative aimed at unlocking private funding for climate-related projects. The fund will invest in green bonds from emerging market financial institutions, which on-lend the funding to climate-related projects in emerging markets. Credit enhancement is provided via IFC investing in a junior tranche amounting to 6.25% of the total fund.

MDBs’ sovereign loans could be potentially more challenging to pool and redistribute, compared to commercially-priced MDB non-sovereign loans and commercial banks loans. One challenge in pooling and redistributing sovereign loans to private investors is the wedge between MDB loan pricing and commercial loan pricing and the issue of preferred creditor status. While a clean sale of such sovereign loans would not involve a transfer of preferred creditor status, it may have to be done at lower than book value. This problem dissipates over time with better investor risk perception of developing countries and as implementation of the Proposals take effect. Sovereign loans can be pooled for investment at a later stage when commercial pricing and MDB pricing narrows.

In the course of the EPG’s consultations, a large body of feedback was solicited on tapping private capital markets and creating an asset class. This feedback can be summarized in the following key considerations for building a successful asset class:

-

Communicate clear commitment to build a credible asset class: Investors will need certainty that the asset class being offered is part of a durable commitment by MDBs to engage with and support market development.

-

Standardize loan contracts and criteria: Standardized loan documentation and disclosures would enable loans from across the MDB system to be packaged together more easily and help attract private investment. MDBs will also need to agree on a common underwriting framework for loans to be eligible for investment by private institutional investors, and also address investor expectations of ‘permissible investments’ and credit enhancements (e.g. guarantees, over-collateralization, liquidity facilities).

-

Build a broad database on loan performance: For developing country infrastructure to become an established asset class, data on the underlying assets must be more readily accessible to build investors’ comfort level and familiarity. Greater transparency85 would also enable MDBs to engage regulators and credit rating agencies in a coordinated fashion, analyze the data to identify key risks that are preventing investments, and develop risk mitigation products to address these risks.

-

Start with a small pilot, then scale up: For a start, two or three MDBs (partnering with private financial institutions) could be tasked to manage a pilot pooled program. Working with the MDBs, the investment community and credit rating agencies, the program manager(s) would decide on the investment vehicle structure, criteria for pooling assets, and the capital structure. In the longer term, pooling assets across institutions for greater diversification benefits should be considered.

Annex 3: Preparing for Pandemics and AMR-related Public Health Emergencies

Pandemics and public health emergencies are high-probability, high-risk events the prevention of which are severely underfunded. The annual global cost of pandemics is estimated at US$570 billion, or 0.7% of global GDP. Growing interconnectedness has increased the risk of national or regional events spreading globally quickly.

These threats require global as well as local and national responses to ensure early detection and adequate response facilities at the global level and within countries. This requires global financing that can be directed nimbly and swiftly, as well as stable funding to boost existing health systems in developing economies, especially those experiencing fragility. The nature of the desired response, of course, would depend on the pandemic, but would require global intervention to develop vaccines and treatments using primarily national delivery systems.

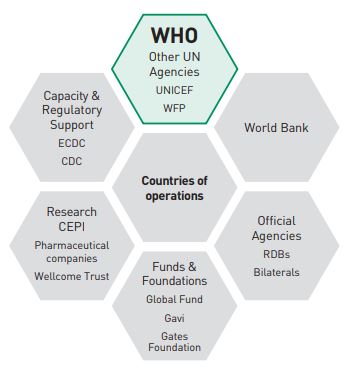

The current global architecture of readiness for public health emergencies has recently coalesced, but still is not fully fit for purpose. A succession of pandemics, most recently the outbreak of Ebola, and the specter of Antimicrobial Resistance (AMR) driving dangerous outbreaks have spurred efforts to organize the system and develop fit-for-purpose financing mechanisms (see Figure 1 for an outline of the actors involved):

-

The bulwark of the system to protect against pandemics and AMR must be the development of domestic health systems with the countries taking ownership. The international community – MDBs, especially the World Bank, bilateral agencies, foundations, and the vertical funds – would need to provide financial and non-financial support.

-

WHO plays the role of guardian of the effort to control pandemics and AMR, identifying global health emergencies and organizing the immediate response by other UN agencies, vertical funds, official agencies and foundations to provide medicines, other supplies and services.

-

The World Bank leads the effort to organize contingent finance through insurance financed by bonds and derivatives, a cash window, and future commitments from donor countries for additional coverage.

Building this emerging structure into a durable and fully effective international response to global health emergencies will require strong action within countries and collaboration among countries, IFIs and the UN agencies with the WHO at the center. The first line of defense against global health emergencies is building country health systems with the support of MDB country programs integrated with funding from donors, foundations and the vertical funds. In support of WHO’s role as first responders, the IFIs also must invest in data, knowledge and analysis for risk identification and mitigation to help countries build resilience and reform programs.

Recent efforts to establish the new pandemic financing vehicles have led to a viable framework, but the system remains vastly unfunded. There is a need to:

-

Scale-up the Pandemic Emergency Facility, which has proven to be a cost-effective approach, as its resources are inadequate considering potential estimates of a full-scale emergency.

-

Enhance existing contingent resources to enable a rapid disbursement of grant resources in response to a crisis either directly to countries impacted or to international first responders.

Figure 1: Global Health Architecture: Structure and Relevant Agencies

Annex 4: Illustrative Institutional Roles for Risk Identification

Note: The roles below reflect the comparative advantages of the IMF, FSB and BIS in the various dimensions of risk identification. They are purely illustrative and not intended to be confining.

| Credit Risk | Market and Liquidity Risk | Country Specific Risk (e.g. Emerging Market) | Macroeconomic Risks | |

| Monetary Conditions | [IMF] Implications of loose/tight monetary policy | [IMF/BIS] Market interest rate deviations from interest rate parity | [IMF] Funding at risk: capital inflows [BIS]Inter-bank (cross-border) flows | [IMF] Adequacy of macro policies (e.g. overheating) |

| Regulatory Conditions, and Intermediation Environment | [FSB] Adequacy of prudential standards for credit (e.g. capital requirements) [BIS] Resilience of market infrastructure [FSB/BIS] Scope and impact of shadow banking | [FSB] Adequacy of capital and liquidity coverage ratios [BIS] Resilience of market infrastructure [FSB/BIS] Scope and impact of shadow banking | [FSB] Aqequacy of buffers [BIS] Inter-bank (cross border) flows | [IMF/FSB] Overall financial stability e.g. FSAP process |

| Financial Conditions | [IMF] Macro-fin: credit cycle in line with economic developments; leverage [BIS] Inter-bank (cross-border) credit exposure | [IMFBIS] Excess liquidity, willingness and capacity of banks to lend | [IMF] Funding at risk: capital outflows; debt sustainability [BIS] Inter-bank (cross border flows) | [IMF/BIS] Overall financial stability |

| Risk Appetite | [IMF/BIS] Asset price developments and investor behavior | [IMF] Willingness of intermediaries to adjust portfolios | [IMF/FSB/BIS] Assessment of investor behavior (safe haven vs search for yield) | [IMF/FSB/BIS] Assessment of investor behavior (safe haven vs search for yield) |

Annex 5: Possible Options for IMF Funding in Large and Severe Global Crises

This Annex sketches out possible temporary mechanisms through which the IMF can rapidly access a significant amount of liquidity to ensure financial stability in the event of a global ‘tail risk’ event. However, a period of consensus building is needed to overcome the governance and policy challenges described below. The EPG is hence not proposing a solution for endorsement at this stage.

Option 1: On-lending of unused SDRs from member country savings

The IMF membership holds substantial SDRs with the IMF (i.e. positive balances), currently amounting to approximately US$150-200 billion. Positive balances could be activated for IMF program lending purposes during times of heightened stress. Interested surplus countries would temporarily lend SDRs to the IMF or a special purpose vehicle, administered by it, at an appropriate fee and incentive structure.86 The additional firepower would correspond to around US$200 billion at maximum, possibly supporting programs in smaller to medium-sized countries (or programs with strong RFA components which the IMF is partnering with). This option could be an additional line of defence and complemented with other options in case of a full-fledged tail risk scenario.

Option 2: Market borrowing by the IMF

Market borrowing, with or without using SDR allocations or existing SDRs as equity, could be operationalized through a cooperative arrangement between the IMF and members to leverage their reserve assets (or issue own SDRs) to constitute a special purpose vehicle that would then issue highly-rated securities on global capital market. This has some parallels with the approach taken by the European Stability Mechanism (ESM) to leverage the capital contributions from Eurozone countries through market borrowing. Applying an illustrative (conservative) leverage ratio of five times for the IMF – the current leverage ratio of the ESM is about six – would yield up to US$1 trillion additional resources from existing dormant SDR balances. Against this backdrop, the IMF’s Articles of Agreement allow the IMF to borrow on the market.

Market borrowing by the Fund faces important governance challenges. First, in the case of SDRs being used as equity by a vehicle that borrows on the market, the preservation of the reserve asset status of the SDRs held by central banks will need to be addressed. Moreover, the regulatory and fiscal treatment of capital contributions by the membership will need to be examined to ascertain permissible use of allocations. An alternative to this mechanism would be for the IMF to use its balance sheet to access the market directly – as allowed by its Articles.

Option 3: Replenishing NAB, and expanding it when needed

Coalitions of the willing have been mobilized in the past and while a repetition in the future is not guaranteed, experience has shown that countries are prepared to come together with additional resources, if needed, to overcome global challenges. There is merit in not phasing out existing arrangements and consider contingency plans for rapid expansions, which should include triggers depending on the severity of systemic crises.

Annex 6: Illustrative Agenda for the G20-led Group of Deputies

The G20-led Group of Deputies (Proposal 18) should endorse the strategic directions and priorities for the MDBs as a system. In the initial stages, the focus would also be on tracking the implementation of the proposed reforms to the system. The key priorities would include: (i) strategic guidance on the risk appetite appropriate to MDBs’ roles in achieving development impact; (ii) ensuring strong system-wide collaboration, including through country platforms which leverage on the strengths of all development partners, and convergence around core standards; and (iii) tracking the shift in business models, and mobilization of private finance through system-wide initiatives.

Decision-making and accountability will be enhanced by developing and refining a system of common metrics amongst MDBs for (i) the planning, monitoring and execution of projects; and (ii) sound risk management. It will require establishing common principles and indicators upon which efficiency and effectiveness of the MDBs should be assessed enabling:

-

A better measurement and tracking of key outcomes and results, including value for money.

-

Comparisons across the MDBs while taking into account their roles in different areas – including geography, knowledge creation as well as over the project and development cycle.

-

Establishing a common statistical base.

The Group should endorse the core development standards underpinning country platforms and leverage on the shareholders represented in the Group to promote convergence to those standards across MDBs and bilateral development finance agencies.

Risk management practices will have to develop significantly for MDBs to embrace the proposals in this Report. The Group should establish a framework to be used by the individual MDBs to specify the risk appetite acceptable to shareholders and the development impact expected, and the trade-off between the two. Implementing this common risk management framework will enable the MDBs to:

-

Make decisions to take higher risk for higher development return, within an overall risk envelope.

-

Implement system-wide risk pooling and diversification, including insurance, aimed at mobilizing much higher levels of private capital.

-

Collectively seek guidance from the Basel Committee and engage credit rating agencies on capital and liquidity requirements, taking into account the MDBs’ unique characteristics and default experience.