Finance

Securing the Benefits of Interconnected Financial Markets: Reforms for Global Financial Resilience

A decade after the global financial crisis, further reforms are needed to reduce the bouts of instability that set back growth, keep countries on the path toward openness and avert another major crisis.

First, to get the full benefits of cross-border capital flows by strengthening support for countries inbuilding deeper domestic financial markets (Proposal 10); and developing and evolving a framework of policy guidance that:

-

Enables countries to utilize international capital flows without risks arising from excessive market volatility (Proposal 11)

-

Enables domestic objectives to be achieved in the sending countries while avoiding major spillovers

Second, to create a more robust, integrated system of risk surveillance (Proposal 13) of a complex, interconnected global financial system, and systematically incorporate contrarian views

Third, to create a strong and reliable global financial safety net by (Proposal 14, 15, 16) stitching together its fragmented layers.

A. GETTING THE BENEFITS OF INTERNATIONAL CAPITAL FLOWS WITHOUT RISKS ARISING FROM EXCESSIVE MARKET VOLATILITY

A key goal of the international monetary and financial system (IMFS) must be to facilitate investments that allow countries to achieve their full growth and development potential, while meeting the needs of savers worldwide.

Achieving this requires a stronger enabling environment, both domestic and international. In particular, it requires stronger domestic financial markets in developing countries, so as to mobilize greater domestic savings as well as utilize global savings in the most productive ways, especially in long-term investments. Equally, we must find ways to mitigate excessive financial volatility, especially that associated with short-term capital flows, and reduce its effects on domestic economies.

Focusing on these two priorities will strengthen the resilience of the system, and address two pressing international challenges:

-

Helping developing countries to break out of recurring cycles of instability that hamper growth: inadequate long-term investments and overdependence on short-term flows; vulnerability to sudden shifts in global risk sentiment and capital flows; and consequent instability that deter long-term investment. Reforms to the IMFS, together with efforts to strengthen countries’ investment environment, must enable developing countries to run sustainable current account deficits where they are fundamentally needed to achieve their full growth potential.

-

Enabling savers, especially in populations that are ageing and seeing extended longevity, with opportunities to diversify risks and earn reliable long-term returns.

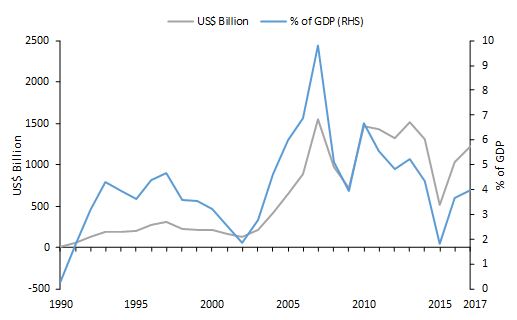

The post-World War II experience of industrialized countries demonstrates that openness, particularly to trade and foreign direct investment (FDI), has brought substantial benefits worldwide, contributing to enhanced physical and human capital and the rise in living standards. Capital flows have also grown significantly for emerging and developing countries over the last 15 years (Chart 1) and offer considerable potential to countries that can utilize them effectively. In particular, FDI has been a major force in the spread of knowledge and best practices in all economies, and an effective engine for growth and development.

Chart 1: Non-resident Net Capital Flows to EMDCs*

Source: IMF

* This comprises FDI, portfolio investment, derivatives, and other flows, including cross-border banking flows.

Countries with deeper domestic financial markets and credible macroeconomic strategies have been best able to catalyze local and foreign financing for development, while demonstrating greater resilience to financial shocks when they occur.

However, spillovers from policies in major economies and shifts in global risk appetite have led to surges or sudden stops in capital flows, and bouts of excessive volatility in exchange rates and domestic asset markets (See Box 3). These fluctuations can interfere with sound policy-making or lead to interventions that hurt growth. The sources of such instability include deviations from sound policies in either sending or receiving countries for capital flows, as well as the structure and technologies of today’s global markets.

Policy thinking on the issue has often been shaped by whether one sits in sending or receiving countries. We need to move beyond this. A rules-based international framework, drawing on a comprehensive and evolving evidence base, is needed to provide policy advice through which countries seek to avoid policies with large spillovers, develop resilient markets, and benefit from capital flows while managing risks to financial stability.

The IMFS must enable countries to benefit from international interdependence and move towards openness as a long-term goal, while managing risks to financial stability. It needs to accommodate economies at each stage of development, and include both sending and receiving countries. In particular, it should:

-

Support countries’ efforts to deepen domestic financial markets, and to tap international markets while managing volatility. This would enable an ongoing liberalization of capital flows at a pace and sequence in line with a country’s circumstances; the OECD’s Code of Liberalization of Capital Movements, originally developed for advanced countries, offers an aspiration in this regard.

-

Develop a regular dialogue aimed at building international understanding around a policy framework for achieving domestic objectives while avoiding large adverse international spillovers that reduce the policy space available to other countries.

-

Ensure the availability of temporary liquidity support for countries with sound policies.

Box 3: Capital Flow Volatility in Emerging Markets

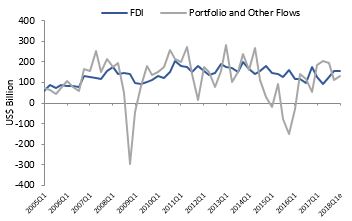

Broadly speaking, capital flows take a few predominant forms: foreign direct investment (FDI), portfolio investments and other flows which take place mainly through banks.

-

FDI has been a major force in the spread of knowledge, techniques and best practices in all markets, and hence an effective engine for growth.

-

Portfolio and other flows play an important role in financing investments, enhancing liquidity in financial markets and enabling risk to be hedged. However, they are significantly more volatile than FDI (see chart) and subject to swings in global risk appetite, besides factors associated with the receiving country.

Non-resident Net Capital Flows to Major EMs

Source: Institute of International Finance

Note: Data captures the 25 largest EMs across Africa, Middle East, Asia Pacific, Emerging Europe, and Latin America.

Surges and sudden stops of short-term flows can lead to sharp bouts of volatility, and may significantly reduce the room for maneuver in policy-making. This is particularly pertinent for emerging markets (EMs), where capital flow volatility has generally been higher than in advanced markets. Those bouts of volatility have also been accentuated by changes in market microstructures and behavior, such as the growth of exchange-traded funds (ETFs) and use of algorithm trading. Further, while aggregate measures of EM capital flow volatility have in recent years been broadly comparable to their mid-2000s average, volatility has increased for many individual EMs, especially among some of the larger EMs.

Studies show that ‘push’ factors (reflecting developments in sending countries and shifts in global risk sentiment) have been playing an increasingly active role in volatility of capital flows and asset prices. At the same time, ‘pull’ factors (e.g. a receiving country’s own policies and circumstances) still explain a significant part of why the impact of a global volatility event varies across EMs.

Proposal 10: The IFI community should strengthen and accelerate efforts to help countries develop deep, resilient and inclusive domestic financial markets.

Deep, resilient and inclusive domestic markets are critical to growth and development and must be a key priority, especially for emerging and developing economies. They help countries to better absorb capital flows and enable an efficient allocation of funds to productive uses in the real sector.

The IMF, World Bank and RDBs should strengthen and coordinate their efforts in partnership with national authorities to meet this need. Capacity building should give emphasis to developing policy and regulatory frameworks for:

-

Sound banking, and local currency debt markets. This should include implementation of prudential regulations as recommended by international standard-setters, which will also reduce risks stemming from capital flow volatility;

-

A strong domestic institutional investor base; and

-

An ecosystem to accelerate financial inclusion through the use of technologies.

Efforts in this regard should tie in closely with the policy recommendations of the framework described in Proposal 11a.

Proposal 11: The IMF’s framework of policy guidance should enable countries to move toward the long-run goal of openness to capital flows and to better manage the risks to financial stability.

A more comprehensive framework of policy guidance is needed to help countries preserve macroeconomic and financial stability, and thereby enable them to make consistent progress towards openness. Experience has shown that countries will only remain on such a path if they can manage episodes of excessive volatility in capital flows and exchange rates and protect domestic financial stability. A framework of policy guidance should help them prevent the build-up of risks in normal times, and to avoid market disruptions and contagion during times of stress

Proposal 11a: Develop evidence-based policy options to enable countries to benefit from capital flows while maintaining financial stability, and to provide assurance to the markets that measures taken are appropriate.

The IMF’s Institutional View should evolve and be extended by bringing several assessments and elements of policy advice together:

-

A comprehensive understanding of the drivers of capital flows and their interaction with monetary, exchange rate and macro-prudential policies;

-

A reliable assessment of the receiving country’s capital flows at risk and macro-financial stability;

-

An assessment of ‘push factors’ from sending countries, especially with regard to the cyclical context and possible reversals; and

-

The Article IV process should develop policy options from the above assessments on how countries can absorb capital flows to mutual advantage, building on evidence on the effectiveness of various tools and instruments, including in particular macro-prudential policies. These options should be updated regularly so that a country has a readily available menu of options in the event of sudden financial pressures.

Over time, adopting such a framework would aim to achieve broad international acceptance. It should also aim at providing assurance to the markets when countries are pursuing a policy mix consistent with the framework.

Proposal 11b: Develop an understanding of policy options that enable sending countries to meet domestic objectives while avoiding large adverse international spillovers.

We need an internationally-accepted policy framework that enables sending countries to adopt their own policies to meet domestic objectives (in some cases set by legislative mandates), while avoiding large international spillovers that reduce the policy space available to others. The framework should evaluate the different domestic policy options with regard to their interactions with capital flows, exchange rates and shifts in global risk appetite. This includes how different policy mixes - including monetary, fiscal and macro-prudential policies - have different implications for international spillovers.

This remains a vexing issue in the IMFS. While ambitious, the importance of such a framework for sustaining support for an open international system cannot be overemphasized.

The IMF should develop this framework, with inputs from national authorities and the BIS. This can be an extension of the IMF’s work on spillovers, and integrated into Article IV consultations for systemic countries.

The policy framework should evolve with evidence and experience. The global adoption and evolution of prudential standards, supported by the G20 and driven by the FSB, is a successful example. Notably, the Basel, IAIS and the IOSCO frameworks - while not mandatory - provide a benchmark to assess the adequacy of financial institutions’ buffers in different countries. Peer and market judgments act as a disciplining device when countries depart from such a framework.

We must build on existing initiatives to develop the needed international framework as described in Proposal 11. The IMF’s Institutional View has been developed to address issues of capital flow volatility and has taken into account countries’ experiences. The Institutional View should evolve and be extended to include:

-

The objective of enabling countries to move toward the long-run goal of openness to capital flows at a pace and sequence in line with country circumstances, while managing risks to financial stability.

-

A more comprehensive framework for evaluating capital flows, including the incorporation of assessments of capital flows at risk, exchange rate policy, and macro-financial stability into policy recommendations. It needs to support countries’ efforts to derive the benefits of maintaining consistent progress on a path to openness, by advising them on the most effective options for managing excessive short-term volatility and its consequences.

The evolved and extended Institutional View should also be complemented by the development of a policy framework that enables sending countries to meet their domestic objectives while avoiding significant adverse international spillovers.

A further need in the global financial architecture is temporary liquidity support for countries with sound policies. Increasing financial interconnectedness has also exposed more economies to significant fluctuations in liquidity, capital flows and risk appetite influenced by global factors, which could reduce their policy space. Evidence shows that flexible exchange rates provide only partial insulation from such fluctuations. Policy makers from emerging economies with sound policy frameworks have hence had concerns that in the absence of predictable sources of international liquidity support, they need to build up further reserves or adopt other policies that will hurt growth.

The liquidity facility should be designed to support good policy-making in countries, and help to reduce incentives to accumulate excessive precautionary reserves. It should also be accessed only in the event of liquidity shocks of a global or regional nature and for a short duration.

The key features of the liquidity facility are set out in Proposal 15.

The IMF’s formal mandate, established in an era when capital flows were small, includes only the current account. On the other hand, the OECD, which has a formal mandate to guide country policies on capital flows, does not have universal membership. There is hence no institution with universal membership that has a formal responsibility to guide countries’ policies on capital flows. This is a lacuna in global financial governance, in a world deeply interconnected by finance, not just trade.

Over the long term, as the IMF and international community build up experience with the proposed framework (Proposal 11), and once there is strong international acceptance developed around its policy advice on capital flows, the goal should be to bring the IMF’s formal mandate up to date to include its role with regard to capital flows.

B. Strengthening Risk Surveillance to Avoid the Next Major Crisis

We will not know exactly where the next crisis will start from. But it will become a full-blown crisis, with broader global consequences, when we are not prepared for it. It is therefore critical that we strengthen our ability to detect risks early, and anticipate how they can be transmitted through a complex and highly interconnected global financial system, so that we can contain them before they escalate.

The official community did not see the Global Financial Crisis (GFC) coming. While the IMF, FSB, BIS and major central banks and regulators have significantly expanded their surveillance capacities, much remains to be done to avert the next major crisis. We should seek to fill the remaining gaps as a key priority, especially in view of current elevated debt levels as well as asset prices, and the prospective tightening of monetary conditions.

Further, the complexity and interconnectivity of the system are continually evolving ‘ with changing business models, new players spread out more widely geographically, and new technologies. Given this rapidly changing landscape, no one international body - the IMF, FSB or the BIS alone - can have a comprehensive grip on the risks in this system. However, existing responsibilities for global financial stability are still too diffused. The last crisis illustrated the consequences.

Proposal 12: Integrate the surveillance efforts of the IMF, FSB and BIS in a coherent global risk map, while preserving the independence of each of the three institutions’ perspectives.

Effective and integrated global surveillance and risk identification will reduce the likelihood of future crises. We must bring the distinct lenses of the IMF, FSB and BIS together, while retaining their comparative advantages ‘ the IMF on economic and macro-financial risks, spillovers and sovereign vulnerabilities; the FSB on financial system vulnerabilities, including the effects of regulatory adaptations and resulting incentives; and the BIS on global flows and market infrastructure. Illustrative contributions by the three institutions are sketched in Annex 4.

The three institutions should develop jointly a global risk map that is continually updated and incorporates the interactions between:

-

underlying macroeconomic and financial conditions, and policy spillovers;

-

the emergence of technology-enabled risks to financial stability , and their implications for an evolving regulatory perimeter;

-

changes in business models of bank and non-bank financial intermediaries ;

-

shifts in the structure of capital markets that may lead to greater pro-cyclicality or reduced ability of markets to prevent large drawdowns;

-

the implications of the above for capital flows and their volatility.

-

the impact of these developments on market infrastructure (e.g. payments, settlement systems and clearing depositories).

These interactions generate risks that only joined-up surveillance can capture. The global risk map would highlight a range of risks and possible pockets of vulnerability with the potential of leading to new crises.

A joint team from the three institutions, - taking inputs systematically from various official and non-official sources but remaining independent in its analysis - should be tasked with developing and continually updating the global risk map. Critically, the process must preserve the independence of the three institutions’ own assessments and staff views, including the appropriate flagging of risks identified by each of them. It must avoid converging on a diluted consensus. While the integrated global risk map would help to synthesize the risks identified by the three institutions, it would also be useful if the joint assessment highlights any differences in perspectives of the three institutions.

Proposal 12a: Incorporate non-official and contrarian views systematically for more robust risk surveillance.

Conventional official wisdom has tended to be behind the curve, particularly in detecting major disruptions in the global financial system. The last crisis was a case in point, where it was the minority view that warned of the coming disruption. Furthermore, given the complexity and decentralization of today’s global financial system, a systematic way of tapping market views and intelligence on potential disruptions is required. The surveillance framework in Proposal 12 should seek out such views.

Proposal 13: Build on the IMF-FSB Early Warning Exercise (EWE) to ensure policy follow-up from the global risk map.

The IMF-FSB EWE should provide the home for policy discussion of global risks among Ministers and Central Bank Governors.

Following from the global risk map (developed through Proposal 12), the EWE should bring together a discussion of risk drivers and outcomes, to raise awareness of both major conjunctural risks and tail risks in the global system. Most importantly, it would facilitate discussions about policy directions and concrete actions to mitigate the key risks and vulnerabilities flagged. Where possible, distinction should be made between risks that require national attention and those that warrant coordinated international efforts, including through further collaboration between the IMF, FSB and BIS.

The exercise should retain the EWE’s closed-door nature, which allows for sensitive assessments and discussion among principals. This will help avoid the risk of triggering market reactions that become self-reinforcing. Nonetheless, in the interest of transparency and accountability, after an initial period the institutions should assess options for disclosure ‘ for example, around the risks identified and recommendations made. This should be in addition to other inputs to the global risk map that are already published.

The IMF should continue to cooperate closely with other relevant bodies, especially the OECD and the Financial Action Task Force on Money Laundering (FATF), to tackle the challenges to the integrity of the global financial system. The threats posed by tax evasion, money-laundering and terrorism financing are ever-present. Further, they could interact with cyber-security risks, and innovations such as new payment platforms and crypto assets that may not be negative in themselves, but together bear close watching and could require tighter global governance in the future.

C. Stitching Together the Fragmented Global Financial Safety Net

Sustaining openness and policies aimed at global growth requires a more predictable global safety net, in which various layers cohere, based on a clear articulation of roles and responsibilities and viable safeguards. Resources should also be adequate and responsive to different stress situations, including systemic global crisis episodes. We do not currently have this safety net.

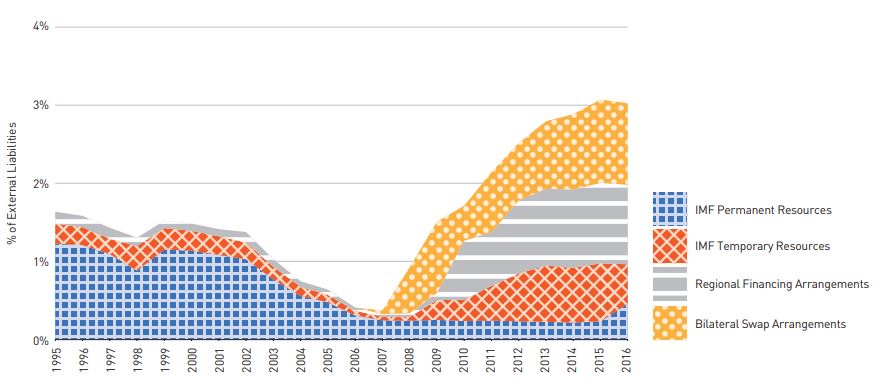

Chart 2: Evolution of the GFSN

Source: IMF and Bank of England

In the last decade, a multi-layered safety net has evolved arising from growth of country reserves, bilateral swap agreements (BSAs) and regional financing arrangements (RFAs). (See Chart 2.) However, the current decentralized structure has several key shortcomings:

-

The safety nets are highly uneven in scale and coverage across regions. About 70 percent of global RFA resources are concentrated in the Euro Area, which has a political underpinning and a common currency that allows the RFA to function quickly and effectively. Other RFAs lack similar underpinnings. There are also large regions which have no access to RFAs, or on any adequate scale.

-

Much of the GFSN’s growth has comprised of BSAs and RFAs which have not been crisis tested, and are subject to conditions prevailing in providing countries and regions. The RFAs and BSAs also do not cover several systemically significant countries.

-

The system as a whole lacks the necessary coordination to effectively use its aggregate financial capacity.

It is therefore critical to have a strong and reliable global layer in the GFSN in place before the next crisis.

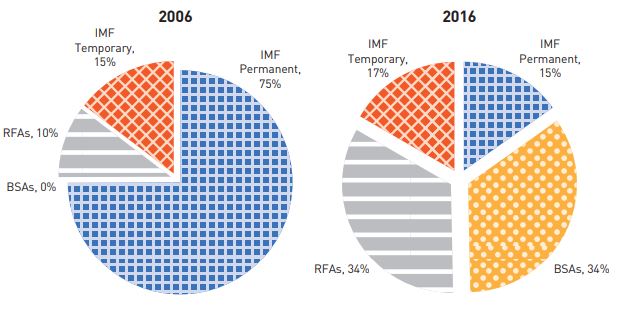

The IMF provides this key global layer in the GFSN. The IMF’s permanent resources (i.e. quotas), supplemented by standing borrowing arrangements (i.e. NAB) should meet the needs of balance of payments crises and contagion episodes in most circumstances and enable the IMF to perform its role as the lender of last resort. Quota and NAB resources thus form the first and second ‘lines of defence’ of the IMF. The IMF also raised bilateral borrowings in the wake of the GFC as a third ‘line of defence’. These combined resources at the IMF equalled 90 percent of total GFSN resources during the 1990s and fell to one-third of total GFSN resources in 2016. (See Chart 3.) When the current bilateral borrowings expire, the IMF’s resource base would fall short of the needs of the global layer of the GFSN that it provides.

Chart 3: Share of IMF Resources Before and After the Global Financial Crisis

Source: IMF and Bank of England

Proposal 14: Stitch together the various layers of the GFSN to achieve scale and predictability.

It is crucial to stitch together the various layers of the safety net well before any major crisis occurs and resources are needed. Effective governance arrangements should encourage sound country policies, and, under specified circumstances, effect joint use of financial resources. A properly designed system, applied in an even-handed manner, can avoid moral hazard, minimize contagion and avoid excessive self-insurance.

No one design will fit all regions. However, a clear assignment of responsibilities between the IMF and each RFA and protocols for joint actions are needed to make the GFSN effective. Work has already begun and should be concluded urgently, respecting key principles as follows:

-

When macroeconomic adjustments and reforms are necessary, GFSN must agree on appropriate ex-post conditionality and avoid postponing adjustment.

-

In case of a temporary liquidity need, without conditionality, the provisions outlined in Proposal 15 would operate.

-

IMF is the most credible and independent party to lead in making these assessments. It alone conducts macro-financial surveillance at a global level and bilateral level, and operates financing facilities which places it in a unique position to provide required assessments.

Proposal 15: Establish a standing IMF liquidity facility to give countries timely access to temporary support during global liquidity shocks.

It is critical that we build and achieve consensus on a ‘standing’ global liquidity facility, drawing on IMF permanent resources (see also Section A). Without a reliable liquidity facility, countries will build up excessive reserves, which will hamper global growth. Timely access to such a facility would also strengthen countries’ ability to withstand liquidity shocks and avoid a deeper crisis.

The facility will provide predictable support to, in line with the IMF’s normal access policies, a set of countries that have been qualified in advance at their request. In the design of this revolving facility, the IMF needs to ensure that: (i) lending decisions follow a separate process rather than being part of an Article IV discussion, thereby maintaining the integrity of the surveillance process; and (ii) the IMF does not act as a de facto rating agency.

This process would give a broad set of countries with sound policies timely access to temporary liquidity support, without the need for protracted negotiations with the IMF. The ability of a country to do so is critical in dealing with ‘IMF stigma’.

Proposal 15a: Use a country’s qualification for the IMF’s liquidity facility in considering the activation of RFA support.

A stitched together GFSN could include parallel activation of temporary liquidity facilities by the RFAs, which would:

-

Leverage each other’s resources to substantially increase the capacity to support their respective membership;

-

Involve a regional layer to address ‘IMF stigma’ concerns, and thereby encouraging countries to access support more promptly.

-

Promote common operating protocols and hence improve speed of crisis response.

Proposal 16: Enable the IMF to rapidly mobilize additional resources in large and severe global crises.

There is a critical need to plug the gap in the GFSN with regard to future crises of a systemic, ‘tail risk’ nature. This requires exploring the possible temporary mechanisms through which the international community can rapidly access a significant amount of liquidity to ensure or restore financial stability.

During the last GFC, around US$500 billion were deployed through the US Federal Reserve’s liquidity swaps with selected central banks. These interventions were critical in ensuring the integrity of the global US$ payment system and in calming global markets ‘ although the majority of emerging market economies did not directly benefit from them. Importantly, such actions cannot be taken as assured in the future.

Furthermore, in response to a joint call by the IMFC and G20, a significant group of countries pledged US$450 billion to temporarily augment IMF resources during the crisis. Participation was not universal. This option of bilateral borrowings for future major crises will require swift mobilization.

There are other solutions that should be explored to enable the IMF to swiftly mobilize resources on the scale requiredto ensure global stability in the event of a major, systemic crisis. The illustrative options are described in Annex 5.

However, while these options are feasible in financial terms, they pose governance and policy challenges (as identified in Annex 5), on which there are differing views. A period of consensus building within the international community will be required for them to be overcome. Consequently, the EPG is not making a proposal for immediate endorsement.

Given the significance of the reforms proposed in this chapter and the key roles of the IMF in effecting them, the IMFC should be regularly updated on the status of their implementation and challenges faced.